Market adoption shifts in 2026

The transition of tokenized loyalty programs from experimental pilots to core enterprise infrastructure has accelerated significantly in 2026. According to market research from Dataintelo, an estimated 78% of Fortune 500 companies with existing loyalty programs are either actively piloting or evaluating blockchain-based tokenization strategies. This widespread adoption marks a definitive shift from speculative testing to structural integration, driven by the need for interoperable, tradable rewards that can operate across disparate brand ecosystems.

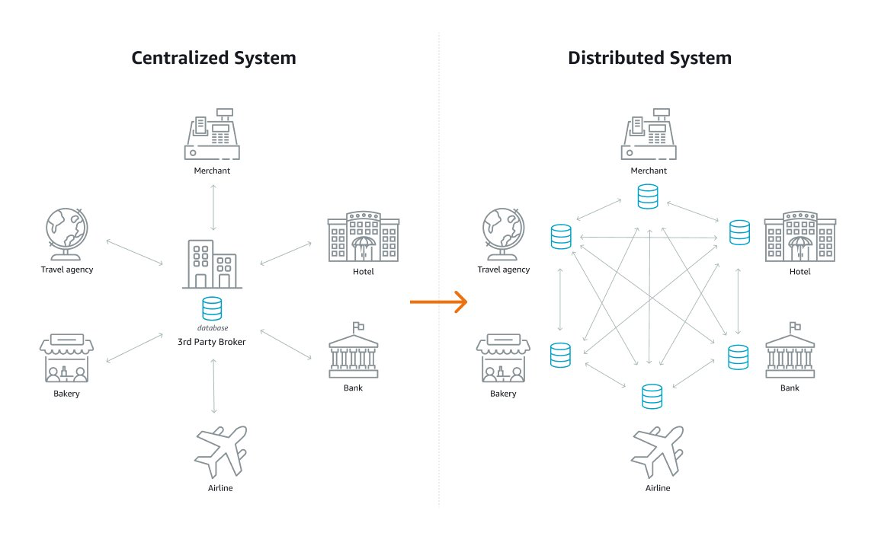

The primary driver for this enterprise uptake is the economic value of liquidity. Traditional loyalty points often suffer from "death by fragmentation," where value is trapped within a single brand's walled garden. Tokenization solves this by converting static points into digital assets that can be traded, pooled, or redeemed across a broader network. This tradability transforms loyalty balances from passive marketing liabilities into liquid assets, fundamentally altering how corporations view their customer retention liabilities.

The market trajectory reflects this structural change. While early adoption was limited to niche crypto-native brands, 2026 has seen traditional retail, aviation, and hospitality giants launch production-ready tokenized programs. This expansion is not merely technological but economic, as brands seek to reduce breakage costs and increase customer lifetime value through enhanced utility. The following chart illustrates the growth trajectory of this sector, highlighting the rapid scaling of tokenized assets from 2024 through the current year.

Tradability replaces static points

The defining structural shift in loyalty programs moving into 2026 is the introduction of tradability. Traditional loyalty programs operate as closed-loop systems where rewards are static liabilities on a brand’s balance sheet, redeemable only for specific future purchases. Tokenized loyalty programs replace these points databases with digital assets that function as transferable property, fundamentally altering the economic relationship between the customer and the brand.

When customers can transfer, sell, or trade their rewards, the perceived value of those points increases significantly. A static point has limited utility; a tradable token has market value. This liquidity allows users to monetize unused rewards or exchange them for other assets, creating a secondary market that traditional closed-loop systems cannot support. As noted in recent academic research on tokenizing loyalty programs, this shift transforms rewards from simple marketing tools into liquid assets with real-world exchange potential.

| Feature | Traditional Loyalty Points | Tokenized Loyalty Rewards |

|---|---|---|

| Transferability | Non-transferable | Transferable via wallet |

| Liquidity | Zero (redemption only) | High (secondary market) |

| Interoperability | Closed-loop (brand-specific) | Open (cross-platform) |

| Asset Class | Liability (unredeemed) | Digital Asset |

This move toward interoperability allows brands to tap into broader ecosystems. Instead of competing for a share of a customer’s wallet within a silo, tokenized rewards can be integrated into decentralized finance (DeFi) protocols or exchanged across different loyalty networks. This structural change pressures brands to offer more compelling, flexible rewards to maintain engagement, as customers now hold actual assets rather than just temporary credits.

Enterprise implementation models

By 2026, enterprise tokenized loyalty programs have moved beyond experimental pilots into structured architectural frameworks. Corporations are selecting implementation models based on their need for liquidity, regulatory compliance, and user engagement depth. The three dominant approaches—utility tokens, NFT-based benefits, and hybrid systems—each solve distinct structural problems in traditional loyalty management.

Utility tokens for liquidity

Utility tokens function as the digital equivalent of traditional points but with blockchain-enabled transferability. Major retailers and airlines issue these tokens to allow customers to trade rewards across partner ecosystems. This model prioritizes fungibility and ease of use. Users can exchange tokens for goods, services, or other digital assets without complex technical barriers. The primary value proposition is liquidity; rewards become an active financial instrument rather than a static savings account.

NFT-based benefits for exclusivity

Non-fungible tokens (NFTs) are deployed to create verifiable, unique membership tiers and limited-edition rewards. Unlike fungible tokens, NFTs represent specific rights or assets, such as lifetime VIP status or access to exclusive events. This model appeals to brands seeking to enhance perceived value through scarcity and ownership. It allows enterprises to offer digital collectibles that serve as proof of status, bridging the gap between physical membership cards and digital engagement.

Hybrid systems for flexibility

Hybrid models combine fungible tokens and NFTs to offer maximum flexibility. Customers might earn utility tokens for daily purchases while receiving NFT badges for long-term engagement. This approach allows enterprises to cater to diverse user preferences within a single ecosystem. It balances the transactional efficiency of tokens with the emotional connection of collectible assets. Hybrid systems are increasingly common among large enterprises aiming to maximize both volume and loyalty depth.

Compliance and Regulatory Risks

Tokenized loyalty programs operate at the intersection of consumer reward and financial infrastructure, a space that attracts intense regulatory scrutiny. As these programs move from closed-loop points to interoperable digital assets, they inevitably brush against securities laws, anti-money laundering (AML) frameworks, and cross-border capital controls. For enterprise adopters in 2026, compliance is not merely a legal checkbox; it is the structural foundation that determines whether a tokenized reward system remains a viable marketing tool or becomes a liability.

The primary legal friction point is the classification of the token itself. If a tokenized reward offers a right to future value, profit sharing, or is marketed with an expectation of appreciation, regulators in key jurisdictions like the United States and the European Union may classify it as a security. The Howey Test in the U.S. and the Markets in Financial Instruments Directive (MiFID II) in the EU provide the frameworks for this determination. A simple discount voucher is generally safe, but a token that can be traded on secondary markets or staked for yield enters the realm of investment contracts. This distinction forces program designers to carefully engineer the utility and restrictability of the asset to avoid triggering full securities registration requirements.

Cross-border transfers introduce another layer of complexity. Unlike traditional points that are often locked within a single jurisdiction’s legal framework, blockchain-based tokens can move across borders instantly. This mobility clashes with local AML and counter-terrorism financing (CTF) regulations. Enterprises must implement robust Know Your Customer (KYC) and transaction monitoring systems to ensure that token transfers do not violate sanctions lists or local capital flight restrictions. Failure to do so can result in severe penalties and the freezing of assets.

The path to adoption requires a proactive legal strategy. Companies are increasingly partnering with licensed custodians and compliance-as-a-service providers to navigate this landscape. By embedding regulatory checks into the smart contract level, enterprises can automate compliance, ensuring that token transfers adhere to the necessary legal standards without compromising the user experience. This structural integration is critical for scaling tokenized loyalty programs beyond pilot phases into mainstream enterprise adoption.

The Future of Loyalty Programs

By 2026, the structural integrity of loyalty programs is shifting from static point accumulation to dynamic, tradable assets. Research from SSRN indicates that tokenized loyalty introduces tradability, allowing customers to exchange rewards for other goods or services rather than being locked into redemption for future purchases with the issuing brand. This shift transforms loyalty points from a marketing cost into a liquid financial instrument.

This liquidity enables hyper-personalization and real-time reward distribution. Instead of generic discounts, brands can offer immediate, context-specific value. As Open Loyalty notes, programs are moving away from traditional points-based systems that are becoming less effective, focusing instead on proving tangible impact through instant gratification.

The economic implications are significant. When rewards become tradable, they compete with other forms of consumer spending. This forces brands to design programs that offer superior utility beyond mere discounts, driving deeper engagement through genuine value exchange rather than habitual point chasing.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!