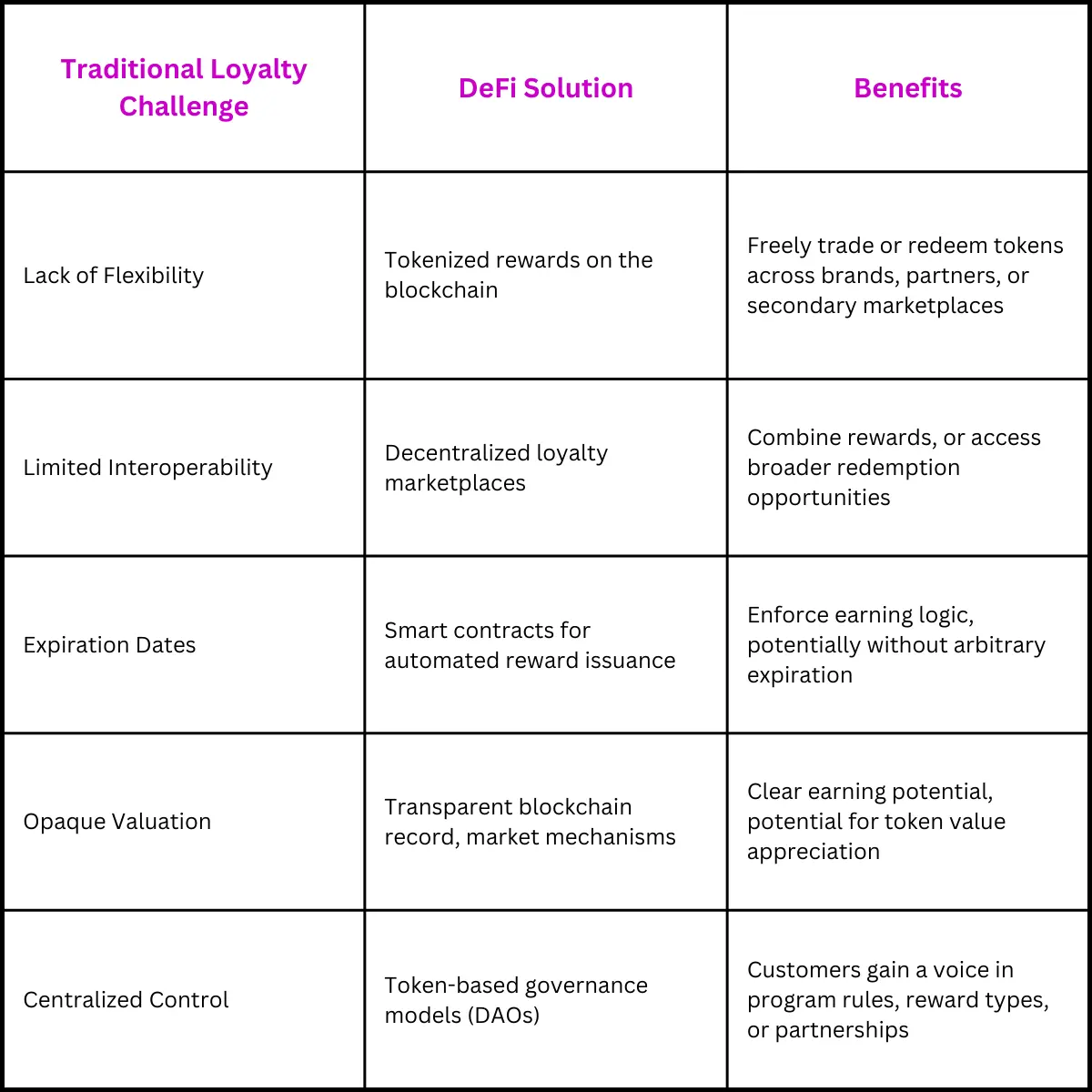

The shift from points to tradable assets

Tokenized loyalty programs 2026 are redefining customer retention by transforming static rewards into liquid digital assets. Unlike traditional closed-loop points systems, where value is trapped within a single brand’s ecosystem, tokenized programs leverage blockchain technology to create interoperable, transferable units of value. This fundamental shift changes loyalty from a liability on a balance sheet into a dynamic asset class for the consumer.

Traditional loyalty programs operate as closed databases. Points accumulate but cannot be exchanged, sold, or used outside the issuing merchant’s specific redemption catalog. This limitation often leads to "points decay" and low engagement, as consumers view the rewards as restrictive rather than valuable. In contrast, tokenized loyalty programs replace these static databases with smart contracts that issue verifiable digital tokens. These tokens can be traded on secondary markets, exchanged for other cryptocurrencies, or used across partnered ecosystems, effectively unlocking real-world liquidity for what was previously dead capital.

The introduction of tradability creates a new psychological contract between brand and consumer. When rewards hold potential secondary market value, they function more like currency than coupons. This interoperability allows customers to maximize the utility of their engagement, whether by holding tokens for appreciation or swapping them for preferred goods elsewhere. As a result, tokenized programs drive higher retention by aligning brand incentives with the consumer’s desire for financial flexibility and asset ownership.

Research indicates that this shift toward tradability significantly impacts customer behavior. A study on tokenizing loyalty programs highlights that the ability to trade rewards reduces the perceived friction of participation, as customers no longer feel locked into a single vendor’s offerings. This liquidity transforms loyalty from a passive accumulation exercise into an active portfolio management experience, fostering deeper brand attachment through economic empowerment.

Why tradability boosts retention metrics

Tokenized loyalty programs deliver a measurable uplift in customer retention, with industry data pointing to a 30% increase in long-term engagement compared to traditional points systems. This improvement stems from a fundamental shift in how rewards are perceived: by converting static points into tradable digital assets, brands transform passive savings into active equity.

The liquidity advantage

Traditional loyalty points are often trapped within a single ecosystem, creating a "closed loop" that limits their perceived value. Tokenization breaks this barrier by introducing liquidity. Customers can trade, swap, or sell their rewards on secondary markets, effectively turning points into a flexible currency. This interoperability, supported by platforms that allow cross-brand utility, significantly increases the utility of every earned reward.

When customers know their rewards hold real-world exchange value, the psychological barrier to leaving a brand rises. The reward is no longer just a discount; it is a liquid asset that retains value even if the customer stops purchasing from the primary brand. This shift from "points" to "property" fundamentally changes the customer-brand relationship, driving higher retention through tangible economic incentives.

Market growth signals confidence

The financial markets are already pricing in this shift toward tokenized engagement. The Tokenized Health Loyalty Programs Market, valued at USD 1.82B in 2026, is projected to reach USD 4.03B by 2030, growing at a 22% CAGR. This rapid expansion reflects not just technological adoption, but a confirmed consumer preference for rewards that offer financial flexibility and transparency.

This growth trajectory underscores the economic reality: when rewards are tradable, they become a core component of the customer's personal financial strategy, making churn significantly less likely.

How to launch tokenized loyalty programs

Launching a tokenized loyalty program requires shifting from simple point accumulation to a digital asset model. This transition demands careful planning across legal, technical, and customer experience layers. The goal is to create a system where tokens function as both rewards and functional utility within your brand ecosystem.

Select a blockchain that aligns with your transaction volume and cost constraints. Public chains like Ethereum offer security but may suffer from high gas fees, while layer-2 solutions or permissioned ledgers provide scalability. Consider the environmental impact and regulatory clarity of your chosen network before committing to a protocol.

Tokens must offer clear value to drive adoption. Determine whether your tokens are utility-based (redeemable for products), security-like (with potential resale value), or hybrid. Establish issuance rates, expiration policies, and transferability rules. A well-designed tokenomics model prevents inflation and ensures long-term engagement rather than one-time speculation.

Address the complex legal landscape by consulting with experts in financial regulations. Tokenized loyalty programs can blur the line between marketing rewards and securities. Implement KYC (Know Your Customer) and AML (Anti-Money Laundering) checks if your tokens are transferable or hold monetary value. Clear terms of service are essential to protect your brand from liability.

Seamless onboarding is critical for mass adoption. Integrate with popular non-custodial wallets or provide a branded custodial wallet option. Enable fiat on-ramps so customers can easily purchase or fund their loyalty wallets. Ensure your e-commerce or POS systems can read and write to the blockchain in real-time to update balances instantly.

Start with a pilot group to test the user experience. Provide clear educational materials that explain how to earn, store, and spend tokens. Use gamification to encourage initial participation. Monitor transaction data closely to identify friction points in the redemption process and adjust the interface for smoother customer journeys.

Implementing tokenized loyalty programs is a structural change that requires cross-functional coordination. By following these steps, brands can build a resilient, engaging, and compliant loyalty ecosystem that stands out in the 2026 market.

Regulatory risks and compliance checks

Tokenized loyalty programs sit at the intersection of consumer rewards and digital asset regulations, creating a high-stakes compliance environment. Unlike traditional points systems, tokens often carry characteristics that trigger securities laws or money transmission regulations depending on how they are structured and distributed.

The primary risk lies in whether a token is classified as a security. If a tokenized reward offers an expectation of profit derived from the efforts of others—such as a brand promising future appreciation or dividends—it may fall under the jurisdiction of the Securities and Exchange Commission (SEC) or equivalent bodies globally. This classification imposes strict registration and disclosure requirements that most loyalty programs are not equipped to handle. Brands must carefully design tokenomics to ensure rewards are treated as utility-based incentives rather than investment vehicles.

Consumer protection is another critical area. Regulators are increasingly scrutinizing the transparency of token terms, including expiration dates, transferability, and redemption processes. Ambiguity in these terms can lead to accusations of deceptive practices. Additionally, anti-money laundering (AML) and know-your-customer (KYC) obligations may apply if the tokens are fungible and tradeable on secondary markets, requiring robust identity verification systems that can friction the user experience.

To mitigate these risks, companies should engage legal counsel early in the design phase. Focusing on clear utility and avoiding financial promises can help keep tokenized programs within the safer bounds of consumer protection laws rather than securities regulations. Regular compliance audits are essential as the regulatory landscape for digital assets continues to evolve rapidly.

Market Outlook and Adoption Trends

The market for tokenized loyalty programs is shifting from experimental pilots to structured growth. Research and Markets projects the tokenized health loyalty programs segment alone will grow from USD 1.82 billion in 2026 to USD 4.03 billion by 2030, reflecting a 22% compound annual growth rate Research and Markets. This expansion signals that major industry players are moving beyond theoretical frameworks to deploy real-world assets as transferable rewards.

Tokenization transforms traditional rewards into blockchain-powered assets that offer real-time settlement and interoperability, addressing long-standing friction in redemption and tracking Photon. As financial institutions like JPMorgan explore tokenized ETFs for near-instant settlement, the infrastructure for tokenized loyalty is gaining similar institutional credibility.

This convergence of fintech infrastructure and loyalty mechanics suggests a rapid acceleration in adoption. Companies leveraging these systems are positioning themselves to capture higher retention rates by offering customers greater control and utility over their earned benefits.

Frequently asked questions about tokenized rewards

What are the main benefits of tokenized loyalty programs?

Tokenized rewards solve the isolation problem of traditional points. Unlike legacy systems where points are locked to a single brand, tokenization introduces interoperability. Customers can use rewards across different platforms and businesses, turning static points into liquid assets. This tradability is the core driver of higher retention, as rewards become more useful and valuable to the holder.

How does tokenization differ from traditional loyalty points?

The primary difference is ownership and flexibility. Traditional loyalty programs treat points as a liability with no transferable value. Tokenized programs issue rewards as digital assets on a blockchain. This allows customers to trade, sell, or swap their rewards for other tokens or fiat currency. It shifts the dynamic from a closed-loop discount system to an open, user-controlled economy.

Is tokenization the next big thing for customer retention?

Institutional adoption is accelerating. Major financial players like JPMorgan see tokenized assets as a transformative force, noting that tokenization enables near-instant settlement and 24/7 access. While the timeline for widespread consumer adoption remains uncertain, the infrastructure is shifting. For loyalty programs, this means the technology is no longer experimental but a viable path to modernizing customer engagement.

Who benefits most from tokenized rewards?

Both brands and customers gain, but the value proposition differs. Customers benefit from liquidity and choice, turning unused points into real value. Brands benefit from reduced liability on their balance sheets and deeper engagement data. The "three R's" of loyalty—rewards, relevance, and recognition—are amplified when rewards are flexible and instantly redeemable across a broader ecosystem.

No comments yet. Be the first to share your thoughts!